Home Owners Insurance Premiums Skyrocketing off the Charts

I’ll apologize and will warn you in advance that this posting may sound more like a wild rant or some serious venting than an informative article of valid real estate information. Regardless, this subject needs some highlighting and attention; I’m just not certain yet what actions will help.

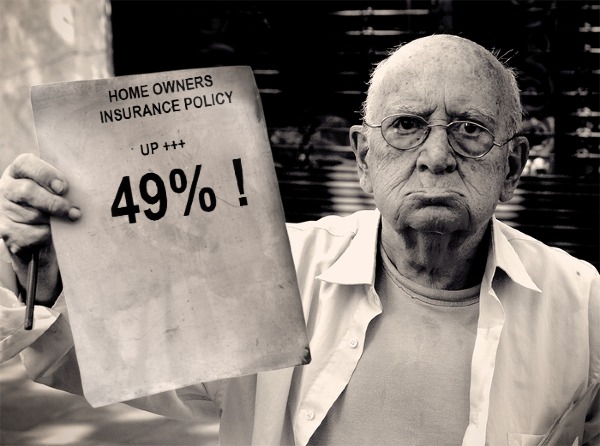

Why all the fuss? I just opened my new Home Owners policy statement this morning and came very close to falling off my chair. By my calculations, my policy premium increased 49% since last year!

After taking some time to collect my thoughts, certainly there had to be a mistake? Unfortunately, a quick call to my insurance agent didn’t help. It was true. His explanation? A higher than normal occurrence of wind and hail damage in the area as well as the on-going reduction in revenues due to foreclosures etc. had forced the insurance company to raise rates to compensate. Seriously?

I’m a businessman and I certainly understand that sometimes situations dictate that the cost of doing business necessitates a raise in prices for services and must be passed on to the consumer – But 49%?, forty-nine percent ! That’s just consumer gouging at its very worst – or company greed at its finest. Unlike other consumer products/services, we don’t really have a choice to carry homeowner’s coverage. Subsequently as well, a few hours of “shopping” other insurance companies didn’t shed a happy ending on the story either. Basically, we’re screwed.

I’m trying to keep a level head. So I thought – we don’t live in a Hurricane Zone, not much chance of a devastating Earthquake hitting the area, mud-slides – wild fires, not likely. Tornadoes – yes, but even then, spread out over a large area with isolated pockets of damage, I can’t imagine that having too devastating of an effect on a company’s bottom line. This is the 2nd insurance issue I’ve had in the past year, the first was with my Auto coverage (not the same company and not something I want to re-hash), and please don’t get me started on health insurance for the self employed unless you really want an earful.

Something is wrong with a business’s pricing model or ethics for that matter when they have to raise rates 49% over the course of several years, let alone, one year. Somewhere we’ve lost the very idea of what insurance is supposed to be. I thought we were partners in rolling the dice together? I give you lots of my money in hopes that I never need to use your services. You (The insurance company) get to keep my money, invest it wisely, keep lots and lots of profits and agree to bail me out and protect me if/when I need it?

Right now, my perception is that it’s become no more than an involuntary tax on homeowners with not much option to avoid. I may be over simplifying the problem and I’m sure I’ll be flamed by some of my insurance agent colleagues but my gut say’s no. So, since this raises the overall cost of home ownership and adds one more layer of complexity to helping fix the housing market, let me focus my efforts on exactly what CAN be done to lower your costs?

- First, if you haven’t already done so, get on the phone with your agent and go over your policy with a fine tooth comb. Leave no stone unturned. I’ve found that many companies have cut way back on things that were covered automatically before (like wind and hail damage for instance). Consider yourself warned.

- Look at the value of your coverage. With home values down considerably over the past few years, many families are still paying for coverage for what their home were worth at the height of the market, not what they’re worth today. This gets a little tricky since home values don’t always match the cost to rebuild.

- Look at your deductable. How likely are you to file a claim against your home? Probably not likely at all so perhaps now especially, it’s time to raise your deductable if it will help. In other cases, consumers are being forced to deal with raised deductibles

- If you haven’t already done so, look to see if combining home and auto coverage will make a considerable difference. In most cases it should, in fact, many insurance companies will ONLY cover you now if you combine both. (this forced requirement is something that doesn’t sit well with me either)

- Shop – Shop and Shop some more.

- Most important of all – File a complaint or forward your thoughts to the Georgia Insurance Commissioner’s office. Most times, consumer apathy is our worst enemy. See: GEORGIA INSURANCE COMMISSIONERS OFFICE

I’m generally interested in hearing some feedback on this subject so I look forward to hearing back from you all.